Today’s housing market is a toxic mix of high mortgage rates, high prices, tight supply and strangely strong pent-up demand — and it’s scaring off buyers and sellers alike.

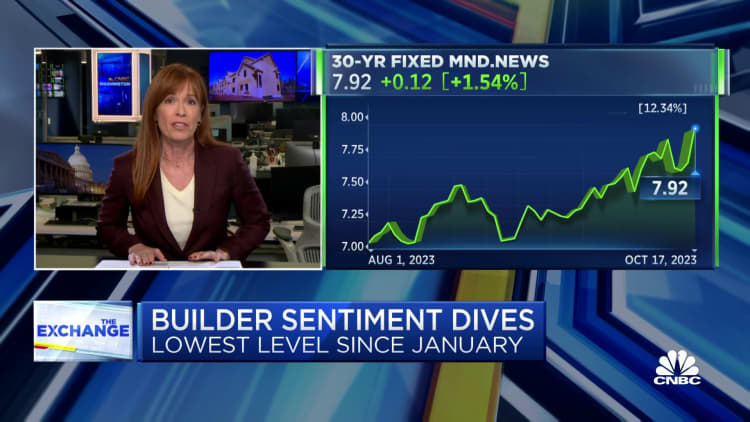

Prices were already high, driven by supercharged demand during the height of the Covid-19 pandemic. Now the popular 30-year fixed mortgage rate is at 8%, the highest in decades, making things even tougher. Mortgage demand is at its lowest point in nearly 30 years.

“I think it’s painful. I think it’s ugly,” Matthew Graham, chief operating officer at Mortgage News Daily, said on CNBC’s “The Exchange” on Thursday.

During the first two years of the Covid-19 pandemic, the Federal Reserve dropped its benchmark rate to zero and poured money into mortgage-backed securities. The result was record-low mortgage rates for two solid years. That drove a buying frenzy, which was also fueled by a sudden urban exodus and the new work-from-home culture. Home prices jumped 40% higher from pre-pandemic levels.

Then, as inflation surged, the Fed hiked rates. That, ironically, made the housing market even more expensive. Usually when rates go up, home prices go down.

But this market is unlike historical ones because it also has a severe lack of supply. The Great Recession of 2008 and the ensuing foreclosure crisis hit homebuilders especially hard, causing them to underbuild for over a decade. They have still not made up the difference.

Who’s hurt by the current housing market?

Would-be sellers, meanwhile, are trapped. They have little desire to trade the 3% rate they currently have for an 8% mortgage rate on a new purchase.

“I don’t think anybody in my community of mortgage originators would disagree that in many ways, this is worse than the great financial crisis in terms of volume and activity,” MND’s Graham said.

He’s also unsure when the market will see a decline in rates. “But we do hear a chorus of Fed speakers, especially last week, in a very notable way, saying that they are restrictive and that they can wait and see what happens with the policy filtering through to the economy,” he said.

Sales of previously owned homes in September dropped to the slowest pace since October 2010, according to the National Association of Realtors. There are stark differences between today’s market and the foreclosure crisis era, however. Foreclosures today are extremely low, and most current homeowners are sitting on historically high home equity. The fact that so many refinanced to record-low interest rates between 2020 and 2022 also means that current homeowners have very affordable housing costs.

So, that leaves potential buyers stuck, too.

“I think people are anxious, and there’s a lot of buyer mentality of, ‘We’re going to wait and see.’ So a lot of people just want to sit tight and see what happens,” said Lisa Resch, a real estate agent with Compass in Washington, D.C.

The NAR is now lowering its 2023 sales forecast to a decline of as much as 20%, from a previous forecast of a 13% drop.

What’s next for housing prices?

Prices are a different story.

“Prices look to be flat from this point onwards at an 8% rate, despite the housing shortage,” added Lawrence Yun, chief economist for the NAR.

Yun noted that metropolitan markets with faster job growth and relatively affordable prices, however, will see an upswing in sales. He points to Florida markets such as Tampa, Jacksonville and Orlando, as well as Houston, Texas, and Memphis, Tennessee.

Buyers today will likely get the best deals from homebuilders, especially the large production builders such as Lennar and D.R. Horton. The builders are helping with affordability by buying down interest rates for their customers. This is something they have not typically done in the past — at least not at this scale.

“Although our mortgage company has been offering slightly below market rate loans most of this cycle (just to be competitive), the full point buydown for the 30-year life of the loan we’ve been referring to recently as a builder incentive is not something we had done in previous cycles, at least not on the broad, majority basis we are doing so today,” said a spokesperson from D.R. Horton. “You might have found it on select homes in the past on an extremely limited basis.”

What about the housing supply problem?

Construction of single-family homes is rising slowly, but it is still nowhere near meeting demand. Builder sentiment is dropping further into negative territory, due to higher rates, but the new home market is still more active than the market for existing homes.

On the bright side of housing, apartment rents are finally cooling off, thanks to a record amount of new supply hitting the market. This gives renters less incentive to jump into buying. Demand for rentals, however, is rising.

“It appears slowing inflation and a still-strong job market are boosting consumer confidence and, in turn, spurring household formation among young adults most likely to rent apartments,” said Jay Parsons, chief economist at RealPage.

For those still wanting to upgrade to a bigger home or downsize to a smaller one, they are caught in a conundrum.

Prices are still rising due to the supply and demand imbalance, but sellers are being more flexible. So a buyer could purchase now at the higher rates and hope to get a break on the price, or they can wait until rates drop.

But when they do, there is likely going to be a flood of demand, resulting in bidding wars.

Read the full article here